Asia, February 2, 2026 — In Brussels Morning Newspaper, the semiconductor industry is moving into a decisive phase of recovery and re-calibration as the global chip market begins 2026 with renewed pricing strength, disciplined supply management, and structurally changing demand patterns. Industry signals emerging across Asia suggest that the sector has moved beyond cyclical correction and into a more balanced phase shaped by artificial intelligence, policy alignment, and long-term capital discipline.

Semiconductor Momentum Builds at the Start of 2026

The opening months of 2026 are reshaping expectations across the semiconductor ecosystem. After enduring a prolonged downturn marked by excess inventories and weak consumer demand, manufacturers are now operating in a tighter, more controlled environment. Supply adjustments made throughout the previous year are translating into tangible pricing power, restoring confidence among suppliers, investors, and downstream manufacturers.

This shift is not driven by short-term speculation but by deliberate strategy. Companies across Asia have re-calibrated production volumes, restructured investment priorities, and aligned output with realistic demand forecasts. As a result, the global chip market is entering the year on firmer footing than many anticipated.

Supply Discipline Becomes the Defining Strategy

One of the most striking changes in the current cycle is the industry-wide commitment to supply discipline. Unlike previous recoveries characterized by aggressive expansion, manufacturers are choosing restraint.

Production lines are being managed with greater flexibility, allowing firms to adjust output quickly without flooding the market. This approach has reduced volatility and contributed to steadier pricing trends. Analysts note that disciplined supply management has become a central pillar supporting stability in the global chip market.

Pricing Power Returns Across Key Segments

As supply tightens, pricing momentum has returned, particularly in components that experienced the steepest declines during the downturn. Contract negotiations entering 2026 reflect renewed leverage for suppliers, especially in memory and advanced logic products.

This pricing recovery is restoring margins and enabling companies to reinvest selectively in technology and efficiency improvements. The result is a healthier competitive environment across the global chip market, where profitability and sustainability are increasingly aligned.

Memory Chips Reclaim Strategic Importance

Memory components remain at the center of the current rebound. DRAM and NAND flash, which are essential across nearly all electronic devices, have seen rapid normalization after months of depressed prices.

Manufacturers have shifted focus toward higher-value memory products while limiting output of lower-margin lines. This re-calibration has strengthened earnings visibility and reinforced memory’s role as a stabilizing force within the global chip market.

Artificial Intelligence Reshapes Semiconductor Demand

Artificial intelligence continues to transform the demand landscape. AI workloads require large volumes of high-performance chips, driving sustained infrastructure investment rather than cyclical consumer upgrades.

Data centers supporting machine learning, analytics, and cloud services are expanding capacity throughout Asia. This structural demand has absorbed available supply faster than anticipated, reinforcing upward pressure across the global chip market.

Inventory Rebuilding Accelerates Procurement

During the previous downturn, many manufacturers reduced inventories to historically low levels to preserve cash and manage risk. As demand visibility improves, procurement teams are now rebuilding stock more assertively.

This restocking phase is amplifying market momentum, as buyers compete for limited availability. Such dynamics are typical during early recovery stages and are contributing to renewed confidence in the global chip market.

Electronics Manufacturers Adapt to Rising Costs

Higher semiconductor prices are prompting adjustments across downstream industries. Smartphone producers, automotive suppliers, and industrial electronics firms are revising cost structures and procurement strategies.

Large corporations with long-term agreements are better positioned to absorb increases, while smaller firms face tighter margins. Despite these pressures, demand for finished products remains resilient, supporting overall stability in the global chip market.

Government Policy Shapes the Industry Landscape

Public policy continues to influence semiconductor strategy. Incentives aimed at strengthening domestic manufacturing capabilities and enhancing supply chain resilience are shaping investment flows across Asia.

While these initiatives support long-term security, they also limit rapid capacity expansion. This controlled growth reinforces supply balance and supports pricing stability within the global chip market.

Capital Spending Returns With Measured Caution

Investment activity is gradually resuming, but with a markedly different tone. Rather than pursuing aggressive expansion, companies are prioritizing efficiency, automation, and advanced manufacturing nodes.

This cautious approach reflects lessons learned from past cycles and supports a more sustainable growth trajectory for the global chip market.

Investor Confidence Strengthens

Financial markets are responding positively to improved earnings visibility. Semiconductor stocks have attracted renewed interest as margins recover and strategic clarity improves.

Investors are focusing on firms with exposure to AI-driven demand, disciplined management, and strong balance sheets. This renewed optimism underscores broader confidence in the durability of the global chip market recovery.

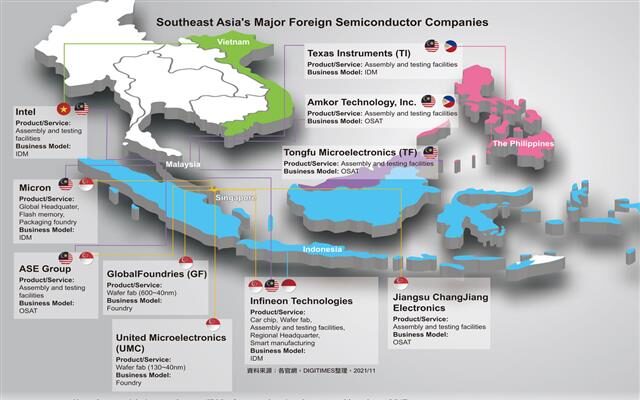

Regional Dynamics Across Asia

Asia remains the epicenter of semiconductor production, with specialized hubs contributing to different segments of the value chain. Foundries, memory fabrication facilities, and advanced packaging centers are all playing critical roles.

Coordination across these hubs is shaping the direction of the global chip market, reinforcing Asia’s influence over pricing, supply, and innovation.

Technology Evolution Drives Competitive Advantage

Beyond pricing, technological advancement is redefining competition. Advanced process nodes, chiplet designs, and energy-efficient architectures are becoming central differentiators.

These innovations are improving performance while optimizing costs, reinforcing long-term competitiveness across the global chip market.

Workforce Challenges and Talent Development

As activity accelerates, demand for skilled engineers and technicians is rising. Companies are investing in training programs and partnerships to address talent shortages.

A skilled workforce is essential to sustaining innovation and operational excellence, both of which underpin long-term success in the global chip market.

Environmental Sustainability Gains Priority

Sustainability considerations are increasingly shaping manufacturing decisions. Energy efficiency, water conservation, and emissions reduction are becoming integral to operational planning.

These efforts align environmental responsibility with cost control, strengthening resilience across the global chip market.

How Past Cycles Shaped Today’s Strategy

The semiconductor industry has experienced repeated boom-and-bust cycles over the past decades. Periods of rapid expansion were often followed by sharp corrections driven by oversupply and collapsing prices.

These experiences have informed today’s emphasis on discipline and balance. By learning from past volatility, manufacturers are adopting strategies designed to stabilize the global chip market and avoid extreme swings.

Outlook for the Remainder of 2026

Looking ahead, analysts expect growth to moderate after the initial rebound. Capacity additions are likely to be incremental, and demand growth may stabilize once inventory rebuilding subsides.

Even so, pricing levels are expected to remain well above previous lows, supporting healthier margins and reinforcing confidence in the global chip market.

One Analyst Viewpoint

A senior semiconductor analyst said,

“This phase reflects a more mature industry, where stability and long-term planning are finally taking precedence over unchecked expansion.”

A Sustainable Phase Takes Shape

The defining feature of the current environment is restraint. Manufacturers appear committed to aligning capacity with demand rather than pursuing market share at any cost.

This strategic maturity suggests that the semiconductor sector may be entering one of its most sustainable phases yet, with the global chip market positioned for steady, long-term relevance.

Beyond Short-Term Cycles

As 2026 progresses, the semiconductor industry is no longer defined solely by consumer electronics cycles. Artificial intelligence, policy frameworks, and sustainability goals are reshaping priorities.

Together, these forces point to a deeper transformation, anchoring confidence that the global chip market is evolving into a more resilient and strategically aligned pillar of the global economy.